Team Tony cultivates, curates and shares Tony Robbins’ stories and core principles, to help others achieve an extraordinary life.

Career & Business

Author and economist Milton Friedman once said, “Inflation is the one form of taxation that can be imposed without legislation.”

Author and economist Milton Friedman once said, “Inflation is the one form of taxation that can be imposed without legislation.”

How to Hedge Against the ‘Silent Tax’ of Inflation

How do we simply define inflation? A “silent tax.” The loss of the purchasing power of your dollar, or more simply put, the amount of goods your dollars can purchase at any given time. And finally, as former major leaguer Sam Ewing says, “Inflation is when you pay $15 for a $10 haircut you used to get for $5 when you had hair.”

What does this mean to you and I? Our savings is effectively shrinking along with our paychecks.

The United States is in a precarious position to say the least. With $16 trillion in national debt and an estimated $100 trillion in unfunded liabilities (Medicare, prescription drugs and Social Security), it seems mathematically improbable for our government to be able to pay for these bills without cranking up the printing press or make drastic spending cuts.

The word “trillions” gets tossed around quite flippantly so let’s break it down to a more digestible example:

If the government were a person, he would…

- Have an annual income of $21,700

- Have an annual spend of $38,200

- Have credit card debt of $160,000

- Have a future impending expense of $1,000,000

BUT in recognition of the problem, he has made total budget cuts thus far of $385.

Inflation, or the possibility of more rapid inflation, is nothing new. In fact, inflation has been an issue since we removed the gold standard. In 1861, the U.S. government suspended payment in gold and silver, effectively ending the attempts to form a standard basis for the dollar. The sum of $1,000 in 1861 is worth $26,300 in today’s dollar when using the CPI index. Keep in mind, the CPI doesn’t take into account energy costs and is a flawed calculation by many accounts. Nonetheless, it does represent a mixed basket of goods and services and tracks the rate of aggregate price changes annually.

So the big question is, what assets have done well during times of inflation? Well, most stock brokers will tell you that stocks have outpaced inflation. Yes, over the very long haul and during certain periods of time they have. Certainly not over the past 12 years with two 40% drops. If you had been wanting to retire in 2009, I would imagine that 2008 changed your plans.

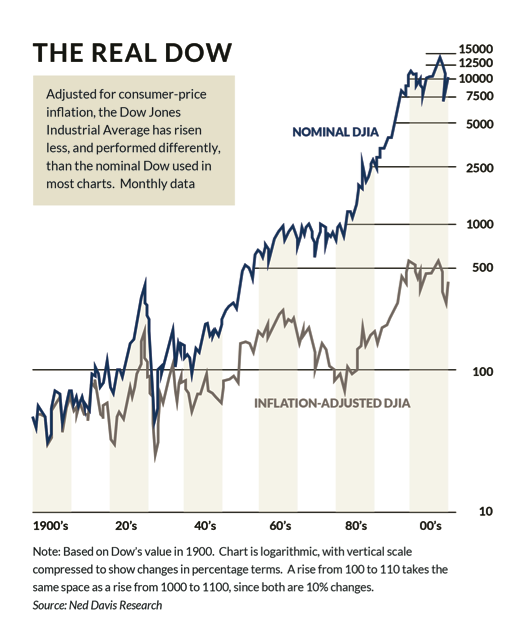

In 2009, during the wake of the 2008 crash, The Wall Street Journal published an article titled “Adjusted For Inflation, Dow Gains Are Puny.” The author (E.S. Browning) was making the basic but important point that you must calculate “inflation adjusted returns.” He points out that “using today’s dollars and starting at 10,520, the Dow would have to surpass 13,460 to get back to its 1999 level in real, inflation-adjusted terms.” At the time of this writing, the DJIA stands at 13,232.

Said another way, when taking into account inflation, the market has basically been flat since 1999.

The chart below shows nearly 100 years of the history of the DJIA in both nominal and real, inflation-adjusted numbers. Quite staggering.

Strategies to Potentially Hedge Inflation

Real estate can be one of more powerful tools to hedge inflation. However, for the first time in history, this last 15 years turned real estate into a paper asset (mortgage-backed securities, CMOs, CDOs etc…) that rapidly created a bubble which ultimately burst. So, this is one area we must have extreme caution and thoughtful analysis.

If this economy turns, commercial real estate could be a bad investment if tenants default or a lack of demand forces prices lower. Historically, residential real estate, with a low interest long-term mortgage, could be a great investment especially if the property nets positive cash flows from rents (assuming it’s not your primary residence).

On the other hand, the challenge with home equity is that it is illiquid, does not provide a rate of return (until it’s sold and realized) and could disappear if we have another housing crisis.

TREASURY INFLATION PROTECTED SECURITIES

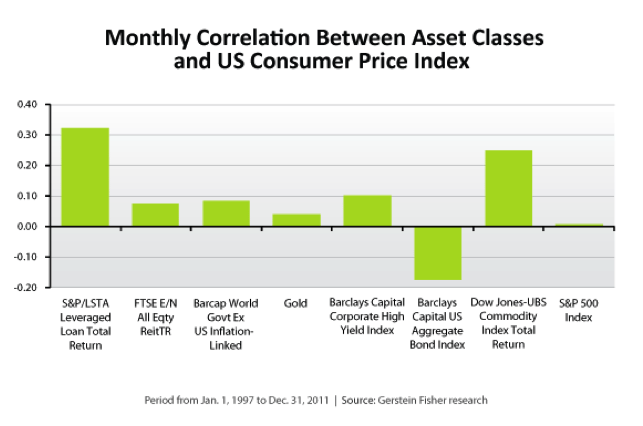

Over time, inflation-indexed bonds have had a positive correlation with inflation (0.08 to be exact). Treasury Inflation-Protected Securities (aka TIPS) are linked to the CPI and thus, if price movements rise, so too will the bond yield/return.

Most people usually invest in TIPS via a fund that is designed to spread the risk across multiple length maturities. However, people tend to think TIPS have no risk, but if you sell them before maturity, or if you own a fund that is weighted with longer-term maturities only, they can have substantial risk.

COMMODITIES

I define commodities as physical assets (vs. paper assets). Commodities include items such as energy (gas, oil), precious metals, industrial metals, grains, coffee, sugar, livestock, etc. For the modern world, it’s challenging to own physical commodities so we are forced to look at other methods such as “futures contracts” which control/own the underlying commodity without actually having possession.

The Dow Jones UBS Commodity Index (total return), a good benchmark for the broad commodities market, has one of the highest correlations to inflation over the past 15 years. It’s not hard to look around and see that gas costs $4 bucks a gallon, gold is over $1,600 an ounce and the cost of food has sky rocketed. Even fresh water is becoming a highly sought after commodity.

The challenge with commodities is their volatility. External circumstances such as weather or war can drastically increase or reduce prices quite quickly.

In part two of this blog series, I introduced a product called a Fixed Index Annuity (FIA) that can provide some substantial benefits, particularly relative to creating a potential inflationary hedge. Like all financial products, a thoughtful analysis is required and no one product or strategy is right for everyone. And because FIAs are offered by many different insurance companies, not all FIAs are created equal.

FIAs generally provide the following benefits:

- 100% of your principal is protected from market decline.

- You earn a fixed rate of interest OR you can forego the fixed rate and link your interest earnings, in part, to the performance of an external market index (i.e. S&P 500). When the index goes up, your interest credits get to participate in the index gains (usually subject to a cap).

- The interest crediting rate will never be less than zero percent, even if the Index goes down.

- When the Index goes up, any interest credits are “locked in,” added to your account value and this amount becomes the new “floor” from which the subsequent year’s interest credits are calculated. Previous “locked in” interest cannot be lost as a result of market decline and the participation in upside market performance is usually subject to a maximum or “cap.”

- Your interest grows without tax until payments are received.

- While there are generally penalties for early withdrawals, there are no annual “management fees” withdrawn from your account value.

At least one FIA allows your interest earnings to be linked, in part, to a commodities index. The composition of the index is 20+ highly liquid futures contracts including physical commodities (gold, grain, oil, gas), global currencies and U.S. interest rates. Over the past 20 years, the worst 10-year timeframe for the index produced an annualized return of 5.08%. The best 10-year segment provided an 8.99% annualized return. Remember, these are the returns of the index itself and depending on how the FIA is structured you would likely receive interest earnings that are slightly lower. And of course, past performance is not an indication or guarantee of future results.

A commodities index can be beneficial in two ways:

- Diversification within the index itself by containing several different asset classes (gold, cotton, energy, global currencies, government bonds, etc.), and

- Generally has an inverse or negative correlation to the traditional stock and bond markets, thus having strong performance during periods of increased volatility, weakness or uncertainty.

In short, you can receive interest credits linked to the performance of commodities within the index as a potential hedge against inflation, but don’t have a corresponding exposure to principal loss tied to poor index performance. Again, this is just one strategy that can help you protect your principal from direct market risk and afford you the opportunity to receive a conservative yet competitive rate of growth on your assets.

TAKING ACTION

Performance Financial, an educational and financial services organization in which I am a partner, provides in-depth education and empowerment for people looking to take control of their financial destiny. Performance Financial Partners is a network of independent advisers and insurance professionals across the country that we have hand-selected for their experience and alignment in philosophy. Over the past eight years, our collective partnership has completed over $5 billion in FIA sales with highly rated insurance companies.

Team Tony